The real cost of credit card EMIs: What you're actually paying

Cost Component

Typical Range / Details

EMI Interest Rate

12%–24% per annum

One-time processing Fee

1%–3% of transaction amount (or a flat fee)

GST on Interest & Fees

18% on both interest and processing fee

Foreclosure / Prepayment Charge

1%–5% of outstanding amount if you close early

Lost Rewards / Cashback

Points or cashback may not apply on converted transactions

Lost Merchant Discount

Discounts for full payment may be forfeited

'Zero-Cost EMI': Free lunch or fine print?

When does converting credit card bill to EMI actually make sense?

EMI vs personal loan vs BNPL: Which one should you pick?

How does converting to credit card EMIs affect your credit score?

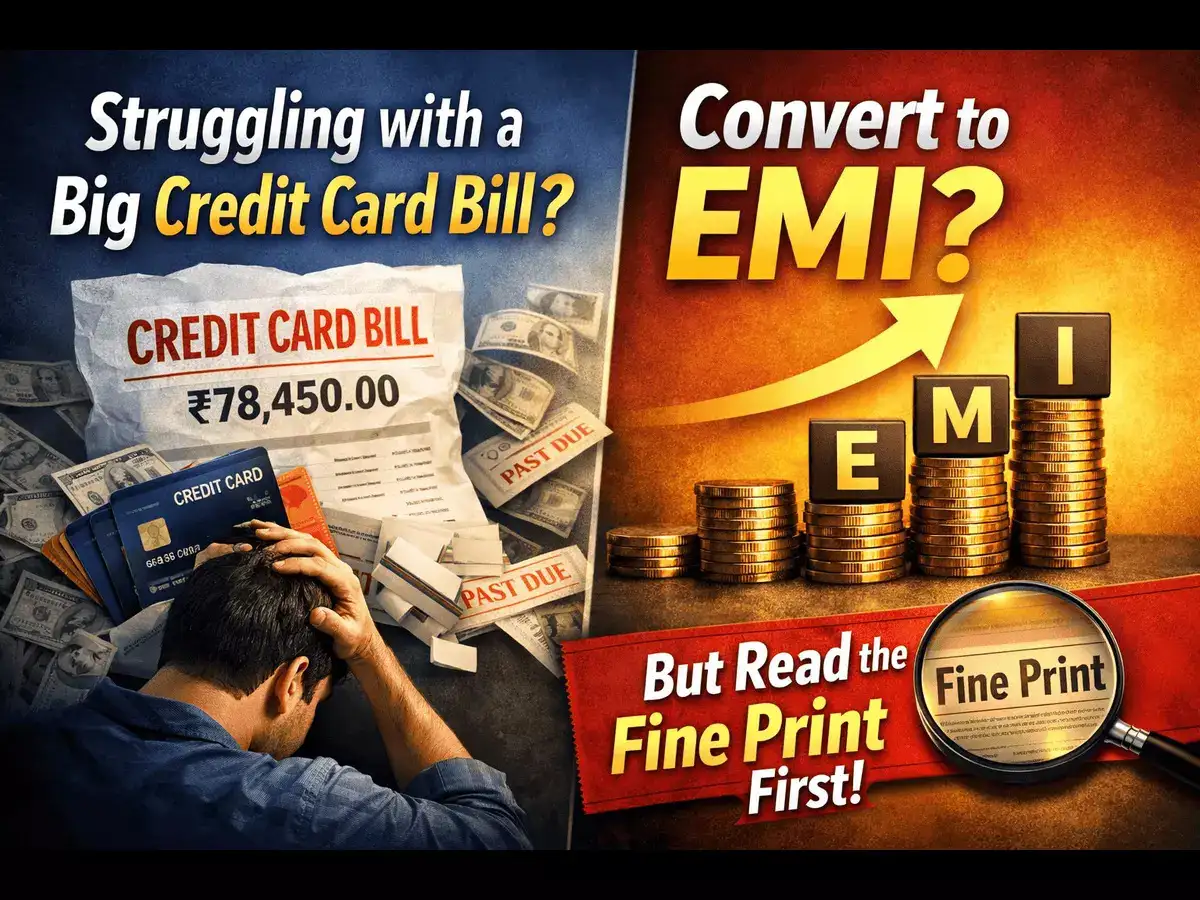

A large credit card bill can feel overwhelming especially when you struggle to clear the dues by next due date. Converting this due into EMIs (Equated Monthly Instalments) often look like the easiest way out. Instead of paying the full amount by your billing due date, you repay it in fixed monthly chunks over a certain period.“When a large number gets broken into small monthly parts, the pain of paying disappears almost entirely. A ₹30,000 purchase converted into a 12-month EMI stops feeling like ₹30,000. It starts feeling like ₹2,800 a month - which feels manageable in isolation,” says Bhargav Errangi, Founder, POP.It is appealing to have smaller payments spread over time that reduce immediate financial pressure but this convenience comes at a price.“EMIs can help when an upfront payment would strain monthly finances,” says Adhil Shetty, CEO, BankBazaar. “However, the cost needs careful evaluation.”The EMI interest rate which is typically between 12% and 24% per annum is only the beginning. Layer in the other charges such as processing fee, GST etc., and the effective cost of your EMI can be significantly higher.“Most banks charge a one-time processing fee, typically 1% to 3% of the transaction or a flat fee. On top of this, 18% GST is applied to both the interest and the processing fee. There are also indirect costs. Consumers may lose out on merchant discounts available on full payment,” says Shetty.Some banks levy prepayment or foreclosure charges if the loan is closed early.“Consumers who try to do the responsible thing and pay early often find a prepayment penalty of 1–3% of the outstanding amount waiting for them. And a missed payment doesn't just carry its own charge - it can trigger the full outstanding balance reverting to standard credit card interest rates, which are significantly higher,” cautions Errangi.'Zero-Cost EMI' offers that come with tags of ‘no interest’ and ‘easy instalments’ sound too good to be true and in many ways, it might be."Zero-cost EMI is often misunderstood. The interest is not eliminated. Instead, it is typically adjusted as an upfront discount funded by the brand or retailer and passed to the bank,” says Shetty.The retailer or brand absorbs the interest cost by sacrificing the discount they would have otherwise passed on to you. So while you don't see an interest line on your EMI statement, you're effectively paying for it through a higher product price.Before opting in, consumers should check whether the product price has been marked up to offset the interest, he adds.“Processing fees and GST may still apply, which can dilute the “zero-cost” benefit,” he highlights.The question isn't whether EMI conversions are good or bad in principle. It's whether they're the right tool for your situation right now.“The underlying test is simple: is this a need that cannot wait? If yes, EMI conversion is a reasonable decision. If the honest answer is no, it probably shouldn't be converted,” advises Errangi.The clearest legitimate cases, include medical emergency healthcare costs are unpredictable, urgent, and can't be deferred. Similarly, an essential appliance that fails, a refrigerator, a work device, may justify a conversion, he explains.If you've already decided you need to borrow, the next question is: which form of credit fits your timeline?"The right question isn't which option is cheapest. It's which instrument matches your timeline," says Errangi.He breaks down the difference between the three most common forms of personal credit,”BNPL works for short tenures - provided you're disciplined enough to clear it within the zero-interest window. Credit card EMIs make sense for three to twelve months; the convenience is real, and there's no separate application to navigate. Beyond that, a personal loan is almost always a better call. The rates are comparable, but personal loans are upfront about the total cost in a way credit card EMIs typically aren't.”Most people make the mistake of choosing credit based on what's most accessible at the moment of purchase, not what's most appropriate for the full repayment period. That mismatch is precisely what turns manageable borrowing into expensive debt.Conversions to EMI affect your credit profile in two important ways: credit utilisation and repayment behaviour.“When a transaction is converted, the full amount is typically blocked against the credit limit. This increases the credit utilisation ratio. Lenders generally view utilisation below 30% as comfortable, while levels above 40% may signal stress,” says Shetty.But the good news is that timely EMI payments strengthen your repayment history and support a healthy credit profile. But even a single missed payment can attract penalties and be reported to credit bureaus, causing a significant dip in your score.Credit card EMIs are one of those financial tools that can either help you manage a rough patch sensibly or quietly lead you into a cycle of rising costs and mounting debt, depending entirely on how you use them.