What exactly is a debt mutual fund, and how is it different from a fixed deposit?

FD vs debt mutual funds: How taxation impacts your returns over time

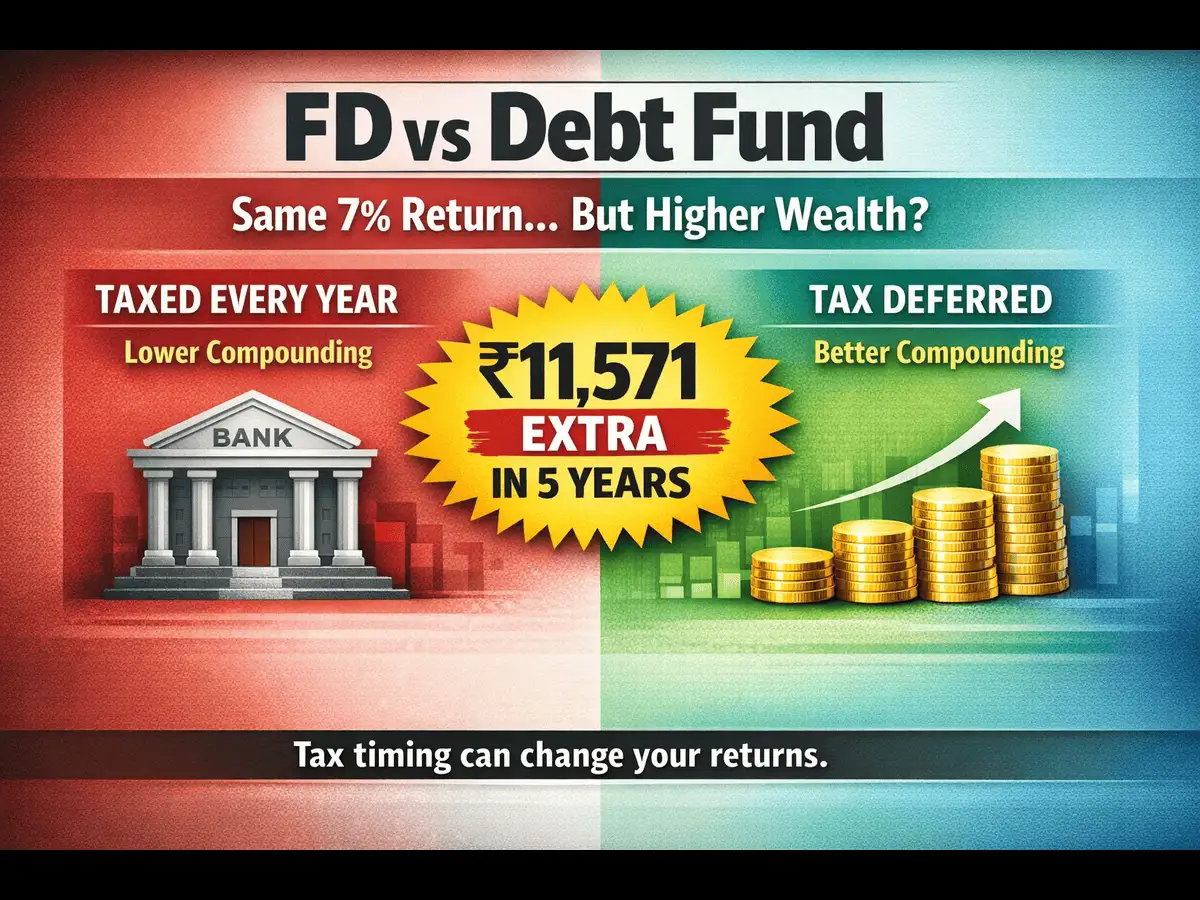

Investment amount: ₹10,00,000

Annual return assumed: 7% (for both FD and debt mutual fund)

Tax slab: 30%

Investment period: 5 years

Investment starts on: April 1, 2023

End of year

Amount invested

FD return (7%)

Tax

Final Value

1

10,00,000

70,000

21,000

10,49,000

2

10,49,000

73,430

22,029

11,00,401

3

11,00,401

77,028

23,108

11,54,321

4

11,54,321

80,802

24,241

12,10,882

5

12,10,882

84,762

25,429

12,70,216

End of year

Amount invested

Debt mutual fund return (7%)**

Tax

Final Value

1

10,00,000

70,000

0

10,70,000

2

10,70,000

74,900

0

11,44,900

3

11,44,900

80,143

0

12,25,043

4

12,25,043

85,753

0

13,10,796

5

13,10,796

91,756

120766*

12,81,786

Debt mutual funds vs FDs: Why tax bracket and investment duration matter

What about risk? Not all debt funds are created equal

For regular income seekers: SWP vs FD interest payout

If you are fed up with market volatility, remember, you still have options that offer stability without completely giving up on returns. For millions of Indian investors, fixed deposits feel safe and familiar.But after taxes, that certainty can come at the cost of lower real returns, often lower than what debt mutual funds are able to deliver, thanks to the power of compounding and deferred taxation where you pay income on your gains only at the time of redemption unlike FDs where you need to pay income tax every financial year irrespective of whether you are withdrawing the interest or not.A debt mutual fund invests your money in instruments like government bonds, corporate bonds, treasury bills, certificates of deposit and other debt instruments. In simple terms, it lends money to governments and companies and earns interest for you.An FD offers a fixed interest rate you already know. A debt fund, on the other hand, doesn’t promise fixed returns. Your investment grows through market value of all debt securities in which the fund has invested and changes in its NAV (net asset value), which can go up or down based on interest rates and many other factors.So, how do you decide which one suits you better? Let’s compare the two.The key difference between FDs and debt mutual funds isn’t how returns are earned, but how they’re taxed.“In case of fixed deposits, the interest earned is taxed every year as per your income slab, regardless of whether you withdraw it or not. Banks may also deduct TDS once the interest crosses the prescribed limit,” says CA Abhishek Soni, CEO & Co-founder, Tax2win. Debt funds purchased on or after 1 April 2023, on the other hand, are taxed only at the time of redemption. And only the capital gains portion is taxed at slab rates, resulting in no annual tax outgo during the holding period (except in case of dividend payouts, if any), he adds.Let’s compare the difference in gains when you park Rs 10 lakh in a fixed deposit at 7% vs a debt mutual fund for a period of 5 years. tax deferral on the same return, the actual returns from a debt fund will vary based on market conditions, interest rate movements, and the fund's portfolio.That translates to a saving of ₹11,571 over five years for someone who chose a debt mutual fund instead of a fixed deposit.This is the single most important concept to understand: tax deferral.When your FD interest gets taxed annually, the taxed-away portion never gets to compound. With debt funds, that money stays in the game, growing and compounding until the day you actually redeem."Compounding is most effective when returns are reinvested without interruptions. In FDs, yearly tax payments reduce the base on which future returns are earned," says Soni. “Over a longer period, this difference can contribute to slightly better wealth accumulation."But the tax deferral advantage isn't equally relevant for everyone. Its impact depends on variables such as which tax bracket you fall in, how much you're investing, and for how long."For investors in lower tax brackets, the difference in post-tax returns between FDs and debt funds may not be very significant," acknowledges Soni.However, for those in higher tax brackets, FDs tend to lose a larger portion of returns due to annual taxation. Debt funds can be relatively more efficient over a 3–5 year period due to tax deferral, though the difference is moderate because the tax is deferred, allowing returns to accumulate before being taxed, he adds.Debt funds give more flexibility, not just in liquidity, but also vis-a-vis when your taxes are triggered."For a large lump sum, the advantage of debt funds is often tax timing and liquidity control," explains Akshat Garg, Head - Research & Product, Choice Wealth. "The investor can stagger exits instead of crystallising everything at one time."At this point, a reasonable FD investor might ask: but aren’t debt funds risky?FDs with scheduled commercial banks are considered relatively safe. Deposits are insured up to ₹5 lakh per bank (Including money parked in FDs, savings, current accounts etc.), failures are rare, and returns are fixed. They do carry some interest rate risk, if rates rise after you lock in, you’re stuck earning a lower return.Debt funds also face interest rate risk, as their values can move with changing rates. In addition, they carry credit risk, the possibility that a borrower in the portfolio may default."The biggest mistake is to treat all debt funds as one category," says Garg.Liquid/overnight funds that stick to high-quality paper are designed for relatively low interest-rate and credit risk, while credit-risk or long-duration funds can be meaningfully more volatile, he says.“So, the right question is not “debt funds are safe or risky?” but “what kind of debt fund, and what is it holding?”,” he adds.One of the most common use cases for FDs, particularly among retirees and those building passive income, is the regular and predictable interest payout.Debt funds offer a comparable structure through Systematic Withdrawal Plans (SWPs).An SWP allows you to instruct the fund to redeem a fixed amount at regular intervals, monthly or quarterly, providing income while the rest of the corpus continues growing."For investors who want income plus control, SWPs are often more elegant; for those who want certainty, FD interest is easier to understand," says Garg. "An FD gives a simple, predictable interest payout. A debt-fund SWP is more flexible, but it is not the same as guaranteed interest."The right choice depends on what you value more: the efficiency of SWPs or the simplicity of FD payouts.For a large number of Indian investors, particularly salaried professionals in higher tax brackets sitting on a growing corpus, the unquestioned loyalty to FDs is costing real money.Debt funds aren’t perfect, and they come with some complexity. But they’re different enough to deliver better post-tax returns for the right investor, over time.Don't compare products in isolation. Look at your tax slab, your investment horizon and run the actual post-tax numbers for your specific situation then choose.