Particulars Till March 31, 2026 From April 1, 2026 Rules and Act Income Tax Act, 1961 and Income Tax Rules, 1962 Income Tax Act, 2025 and Income Tax Rules, 2026 ITR filing due date 31-Jul-26 July 31, 2026 for AY 2025-26 and AY 2026-27 (for ITR-1 and ITR-2). From AY 2026-27, August 31 for ITR-3 and ITR-4 (non-audit), October 31 for audit cases TCS on foreign tours Up to Rs 10 lakh its 5% and 20% rate on above Rs 10 lakh Overseas tour packages: Flat 2% TCS (no threshold) Education/medical remittances: Reduced to 2% Certain goods (scrap, minerals): Increased to 2%. TDS on property (seller is NRI) Simplified TDS for Property Purchase (NRI). Buyers can now deduct TDS using PAN-based challanNo requirement to obtain TAN Buyback of shares Taxed as deemed dividend at your slab rates Taxed as capital gains. For individuals either STCG or LTCG depending upon holding period Revised income tax return (ITR) due date 31-Dec 31-Mar House Rent Allowance (HRA) Earlier, only Mumbai, Delhi, Chennai, and Kolkata qualified for 50% HRA exemption (of basic salary) Now in addition to the earlier four cities, Hyderabad, Pune, Ahmedabad, and Bengaluru are also included Meal card tax benefits Rs 50 per meal Rs 200 per meal Source: S K Patodia LLP

"Tax Year" will replace FY and AY term

HRA claims revised

HRA rule change 2026

Tax benefits on meal cards

Children's education & hostel allowance

Company car perk

Changes in Sovereign Gold Bonds (SGBs)

TDS deduction NRI property

Tax Collected at Source relief on foreign tours

Increased time to file revised returns

No TDS on motor claim

PAN Rule Changes

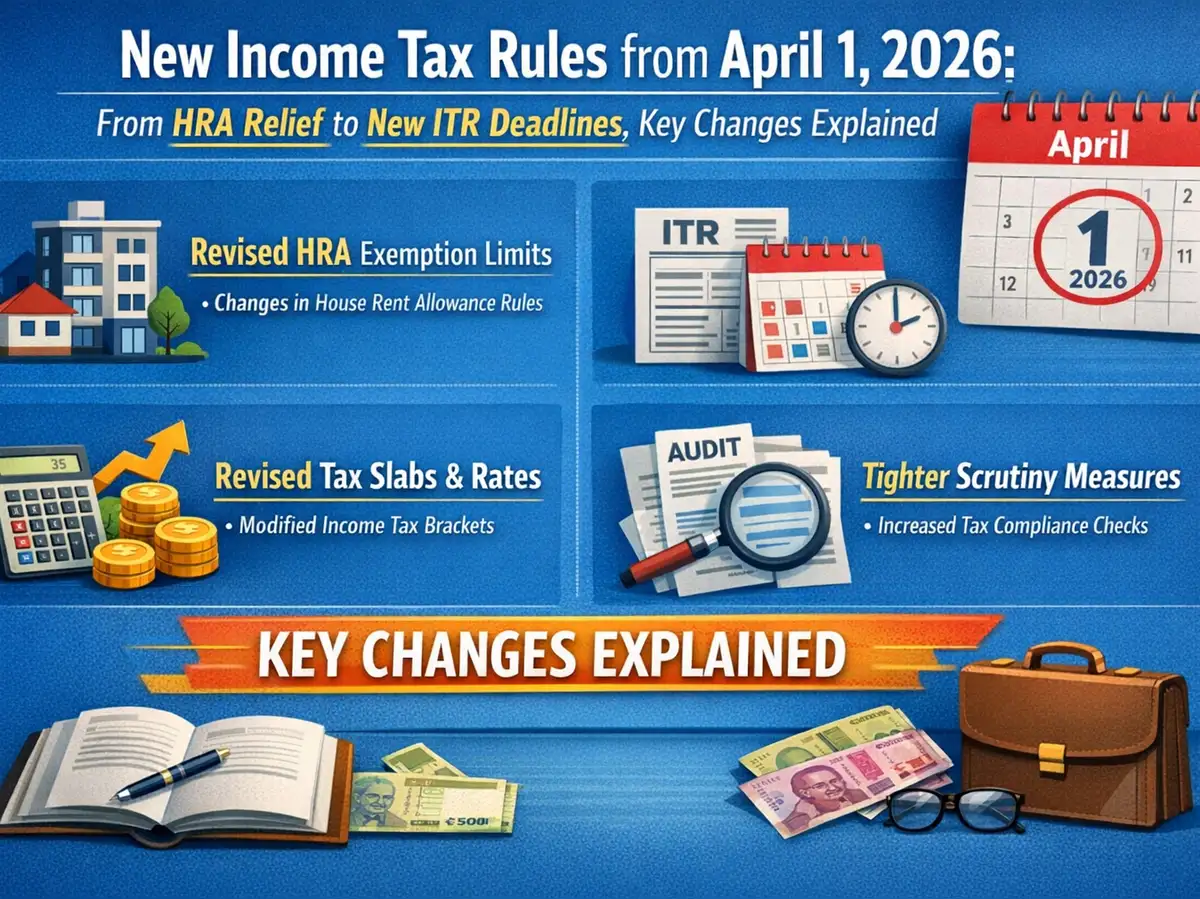

Several important income tax changes are scheduled to go into effect on April 1, 2026 , providing taxpayers with a combination of relief and increased compliance requirements. Howeve, it is important to note that you have to continue with the existing Income Tax Act, 1961 for filing income tax return (ITR) for AY 2026-27.The concept of Tax Year, the newly released forms and new Income Tax Rules will all apply for ITRs to be filed in 2027 for the first Tax Year 2026-27. Kinjal Bhuta, Treasurer at BCAS, said to ET Wealth Online that it is important to note that these changes will come into effect from April 1, 2026, and therefore will not apply to the Income tax Returns being filed for AY 2026-27.Here's a look at the major income tax rule changes that taxpayers should be aware of.For AY 2027-28 i.e. from April 1, 2026 new rules like revised TDS and TCS provisions to changes in income tax return filing timelines, buyback taxation, and new reporting formats, the updates will have a direct impact on tax planning and compliance for FY 2026- 27. Notably, concepts like the introduction of a "Tax Year", revamped income tax forms, and updated deduction limits signal a shift towards a more streamlined tax regime.The Income Tax Act of 2025 will replace the long-standing Income Tax Act of 1961. The Income-tax Act, 2025 has been enacted to provide a streamlined, simplified, and modern tax code with reduced compliance burden, consolidated provisions, and clear definitions.From April 1, 2026 tax rules 2026 and Tax Act 2025 is applicable but for ITR filing for July 31, 2026 which rules and Act is applicable?Hon. Treasurer at BCAS says, "It is important to note that this change will come into effect from April 1, 2026, and therefore will not apply to the Income tax Returns being filed for AY 2026-27. Taxpayers will continue to follow the existing Income Tax Act, 1961 for filing their return for AY 2026-27. The concept of Tax Year, the newly released forms and new Income Tax Rules will all apply for returns to be filed in 2027 for the first Tax Year 2026-27."The phrase "Tax Year" will take the place of the terms Financial Year and Assessment Year. The main aim of this change is to reduce confusion.The income tax return (ITR) filing deadlines have been slightly revised this year. For salaried individuals filing ITR-1 or ITR-2, the deadline continues to remain July 31, with no change. However, for non-audit cases filing ITR-3 and ITR-4, the deadline has been extended to August 31, giving self-employed individuals and professionals some extra time to gather documents and complete their filings without rushing.Taxpayers will need to disclose their relationship with their landlord in Form No. 124 (corresponding to Form No. 12BB) when they pay rent, especially in situations where the landlord is a relative. Employees must now give their landlord's PAN along with proper proof of rent payment. In certain cases, revealing entire landlord details, including PAN and rent amount, is necessary when claiming HRA.Starting April 1, 2026, new income tax rules will expand the list of cities that qualify for higher House Rent Allowance (HRA) tax exemption. Salaried employees who live in these additional cities, going beyond the traditional four, can now take advantage of larger deductions.Earlier, only Mumbai, Delhi, Chennai, and Kolkata qualified for 50% HRA exemption (of basic salary) . Now, Hyderabad, Pune, Ahmedabad, and Bengaluru are also included. If you live in any of these 8 cities, you can claim higher tax relief compared to other locations.Salaried employees who get the benefit of meal coupons, meal vouchers, meal cards (like Sodexo/Pluxee, Zaggle), or subsidised food from the office canteen, can now claim an income tax deduction of up to Rs 1.05 lakh , under both the old and the new tax regime. This arises out of the new Income Tax Rules, 2026 which the parliament approved last week. Earlier, the tax exemption for such meal cards/vouchers/subsidised food was capped at Rs 50 per meal which meant that if your employer provided you two meals a day worth Rs 50 each (totaling Rs 100), then that amount was exempt from income tax.After being stuck at the same token levels for decades, two allowances are set to be revised. The children's education allowance is proposed to increase from Rs 100 to Rs 3,000 per month per child (up to 2 children) and the hostel allowance from Rs 300 to Rs 9,000 per month per child. For a parent with two children in hostels, this alone adds up to Rs 2.16 lakh in annual exemptions compared to just Rs 7,200 earlier.One change may hit employees in both regimes equally. The taxable value of employer-provided cars is proposed to be nearly tripled. Smaller cars (under 1.6 litre engine) might go from Rs 2,700 to Rs 8,000 per month in taxable perquisite value. Larger cars rise from Rs 3,300 to Rs 10,000 per month. There's no relief under either regime and your taxable income simply goes up if your employer provides a car.Starting April 1, 2026, tax-free Sovereign Gold Bond (SGB) redemption solely to original subscribers who hold the bonds until maturity. Secondary market buyers will now face a 12.5% Long-Term Capital Gains (LTCG) tax upon maturity, significantly reducing returns compared to previous rules.Buyers can now deduct TDS on property transactions with Non-Resident Indians (NRIs) using their PAN. This eliminates the previous requirement of acquiring a TAN, making the process easier.Tax Collected at Source (TCS) on foreign tours has been reduced, bringing relief to international travellers. Earlier, TCS was charged at 5% on tour packages up to Rs 10 lakh and 20% on amounts beyond that, but now a flat 2% TCS will apply on the total tour cost,. Similarly, TCS on remittances made for education and medical treatment abroad has also been reduced-from 5% on amounts exceeding Rs 10 lakh to just 2% making overseas education and healthcare expenses slightly more affordable.Taxpayers now get more flexibility, earlier deadline was December 31 (9 months), now the new deadline is March 31 (12 months), 3 months more time.Note that filing after December 31 will attract additional fees. The deadline for belated returns remains unchanged.No tax shall be deducted at source on any interest amount awarded by the Motor Accidents Claims Tribunal to an individual if such interest is credited or paid to an individual.It is no longer possible to apply for a PAN using just Aadhaar. Form 93 for individuals, Form 94 for businesses, Form 95 for foreign individuals, and Form 96 for foreign corporations are the category-specific forms that applicants must now utilise.